Fiscal Strategy Report 2026

Te Rautaki Moni Tūmatanui

The Public Finance Act 1989 (PFA) requires the Minister of Finance to present to the House on Budget Day a report on the Government's fiscal strategy. This must set out the Government's short-term fiscal intentions, long-term fiscal objectives, revenue strategy, and strategy for managing expenditure, assets and liabilities. The report must include scenarios that contain projections of trends in fiscal variables for at least the next 10 years.

This Fiscal Strategy Report (FSR) is released alongside Budget 2026 and draws on the 2026 Budget Economic and Fiscal Update (BEFU). It also makes comparisons with forecasts in the previous update, the 2025 Half Year Economic and Fiscal Update (HYEFU). Key terms are defined in the BEFU glossary.

Fiscal strategy

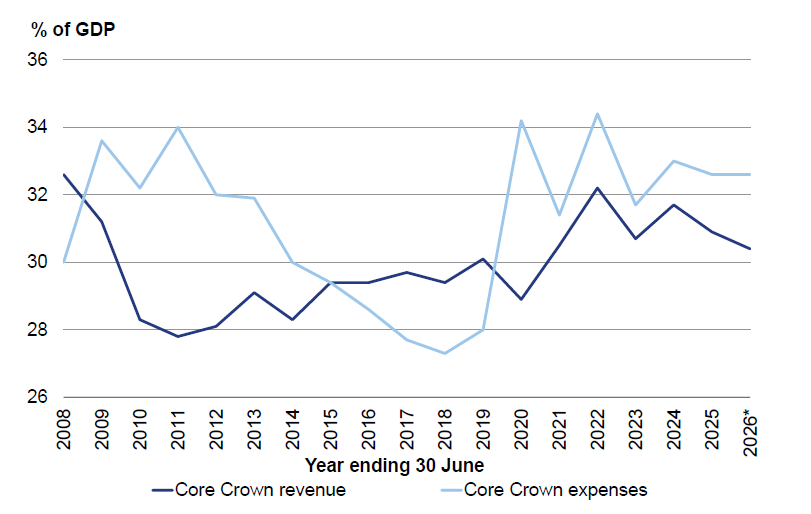

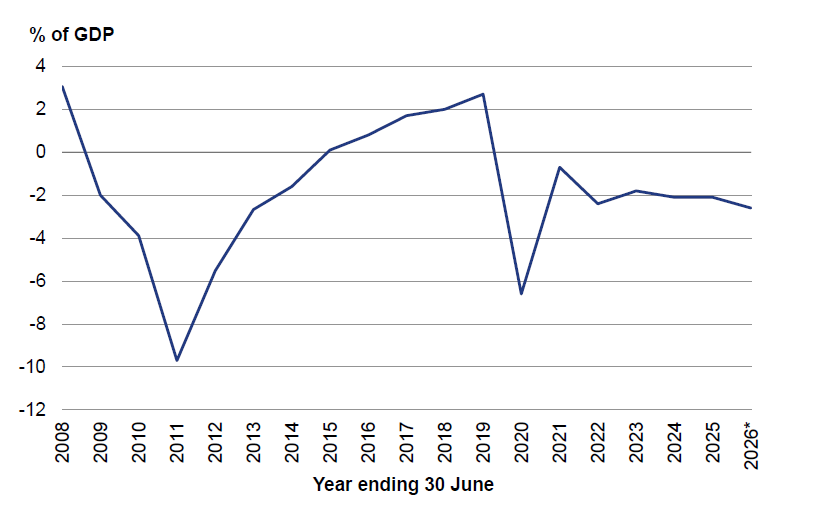

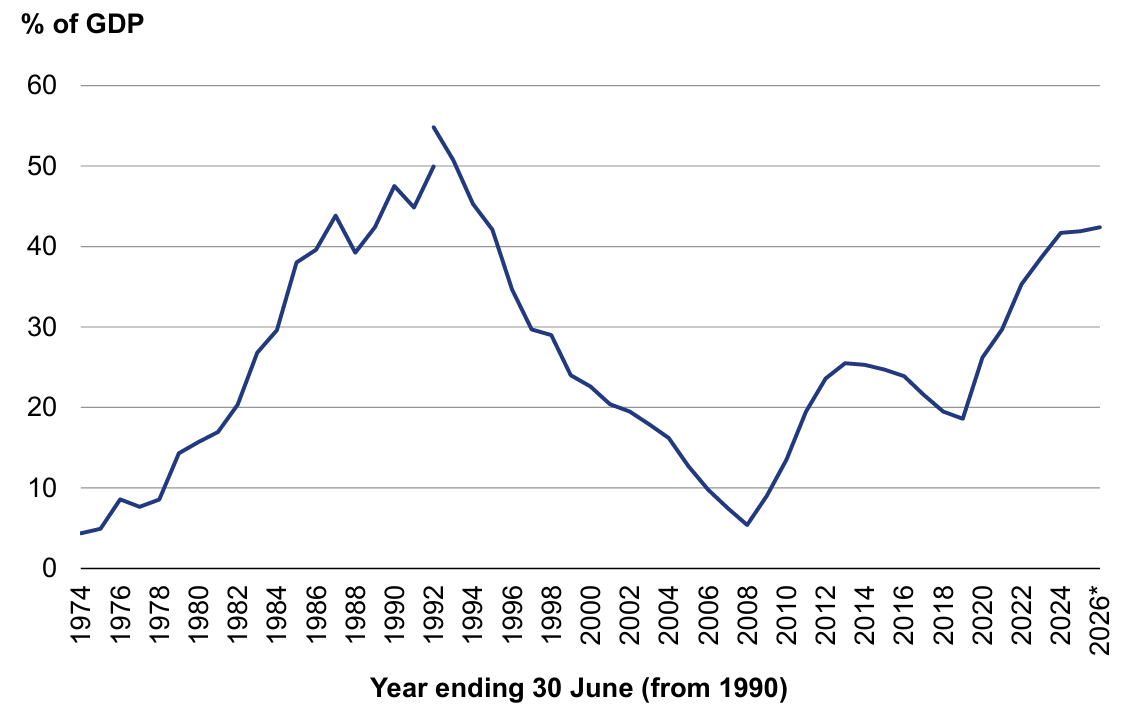

The Government's fiscal strategy aims to repair its books after a period of deficits and debt accumulation. The operating balance before gains and losses excluding the Accident Compensation Corporation (ACC), or OBEGALx, has been in deficit since 2019/20 as core Crown expenses have risen faster than core Crown revenue (Figures 1 and 2). Operating deficits, combined with capital spending, led to a sharp increase in net core Crown debt between 2019/20 and 2023/24 (Figure 3).

Figure 1 — Core Crown revenue and expenses

* 2026 shows the latest forecast

Source: The Treasury

Figure 2 — OBEGALx

* 2026 shows the latest forecast

Source: The Treasury

Figure 3 — Net core Crown debt

* 2026 shows the latest forecast

The measure of net core Crown debt adopted in 2009 is restated back to 1992. The earlier measure for the period before 1992 included advances. March years are used prior to 1990.

Source: The Treasury

The sharp increase in core Crown expenses as a share of GDP after 2018/19 was due to the COVID-19 pandemic and weather events, rising costs of delivering public services, demographic changes, higher borrowing costs, the economic downturn and deliberate decisions to increase spending. Total Budget 2022 new operating spending, for example, was $9.7 billion a year, on average. Table 1 sets out the contribution of different spending areas to the increase in core Crown expenses since 2018/19.

Table 1 — Increase in core Crown expenses from 2018/19 to 2025/26 by functional classification

| Functional classification | $billions |

|---|---|

| Core Crown expenses 2018/19 | 87.0 |

| Health | 14.9 |

| NZ Superannuation | 10.2 |

| Welfare benefits | 9.4 |

| Education | 7.2 |

| Finance costs | 5.4 |

| Transport and communications | 3.2 |

| Law and order | 2.7 |

| Housing and community development | 1.5 |

| Other | 5.7 |

| Core Crown expenses 2025/26* | 147.2 |

* 2025/26 shows the latest forecast

Source: The Treasury

The operating deficit will not resolve automatically as the economy recovers. Fiscal consolidation is required to return OBEGALx to surplus and bend the debt curve down. Lower debt as a proportion of GDP will mean the government is in a better position to absorb and respond to future shocks and economic cycles. Recent decisions by both Fitch Ratings and Moody’s Ratings to change the outlook for New Zealand’s sovereign credit rating from stable to negative reflects this need for fiscal consolidation.

The Government's fiscal strategy is essentially unchanged from that set out most recently in the 2026 Budget Policy Statement (BPS). The strategy is to limit new spending in each Budget, find savings and reprioritisation from within the existing base of expenditure and maintain a deliberate, medium-term approach to fiscal consolidation. This approach avoids a sharp impact on frontline public services and helps support the economic recovery. The Government has always said it would not over-react to changes in fiscal forecasts, so upside revenue surprises, such as those shown in the BEFU, will contribute to reducing the deficit. On the other hand, downside revenue surprises will not necessitate a sharp spending reduction. Specifically, the Government intends to:

- reduce core Crown expenses towards 30 per cent of GDP

- return OBEGALx to surplus by 2028/29, and

- put net core Crown debt as a percentage of GDP on a downward path towards 40 per cent.

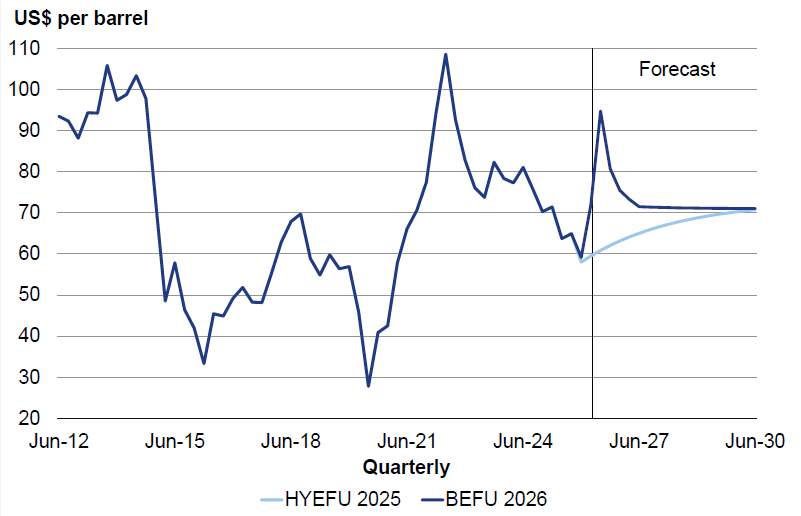

Box 1 — Fiscal response to the Middle East conflict

Conflict in the Middle East has introduced significant uncertainty to the global economic outlook. The conflict has led to higher oil prices, which are forecast to persist in the near term (Figure 4). In the short term, higher oil prices are expected to lead to higher inflation and lower economic growth, globally and in New Zealand.

Figure 4 — West Texas Intermediate crude oil forecast comparison

Sources: Haver Analytics, U.S. Energy Information Administration, the Treasury

New Zealand has a well-established framework where macroeconomic stabilisation — providing or removing stimulus to reduce large swings in the economy — is primarily the responsibility of the independent Reserve Bank. Automatic fiscal stabilisers play a supporting role. These are features of the tax and transfer system, such as increased benefit spending during downturns, that automatically dampen economic ups and downs without needing new government policy decisions. Timely, temporary and targeted fiscal measures can also help take the sharpest edges off an economic shock.

In response to the current fuel crisis, the Government has increased the in-work tax credit by $50 a week for up to a year to provide support to low- to middle-income working families as higher fuel prices add pressure to household budgets. This increase is temporary and carefully targeted to avoid adding to inflationary pressure or government debt. The Budget also provides targeted support to schools, community support workers and essential services to help manage fuel cost pressures. It sets funding aside in reserve for additional temporary fuel-related measures, if required. All fuel response funding has been managed against the existing Budget 2026 operating allowance, to ensure it is consistent with the Government's fiscal strategy.

The PFA requires an assessment of the extent to which the fiscal performance of the Government is consistent with its fiscal strategy report for that period. In 2024/25, the only full financial year since this Government was formed, both core Crown expenses and net core Crown debt were lower as a share of GDP than had been expected in the 2024 FSR. OBEGALx was not forecast at that time, but OBEGAL in 2024/25 was similar to the forecast in the 2024 FSR.