Budget operating and capital allowances

Spending restraint is realised by setting Budget operating and capital allowances.

The operating allowance is the amount of net new operating funding - on average, per annum - the Government intends to spend on discretionary policy initiatives in each Budget. As a net concept, operating allowances include spending, savings and revenue initiatives within a single envelope.

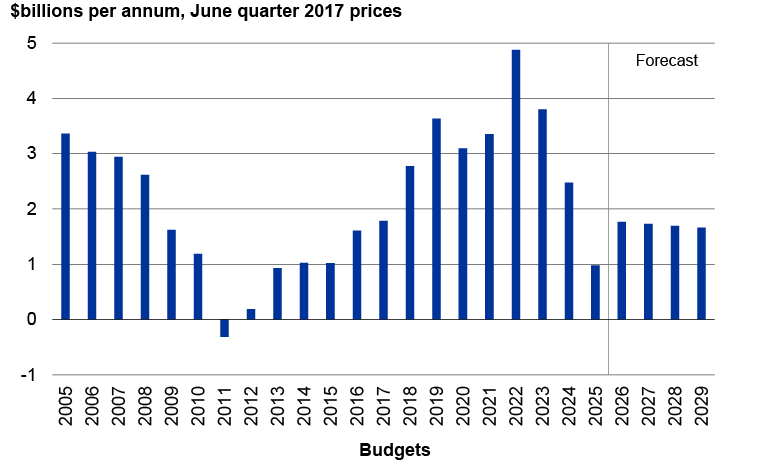

The operating allowances for Budgets 2026, 2027 and 2028 remain at $2.4 billion. The operating allowance for Budget 2029 has also been set at $2.4 billion. These are tight allowances, particularly compared to those for Budgets 2018 to 2023 (Figure 4). While the Government has made its medium-term spending intentions clear by setting allowances at this level, there remains room for some adjustments up or down in the future. Any future adjustments would have to be consistent with the overarching objective to get the government’s books back in order and restore discipline to public spending.

Figure 4 - Real Budget operating allowances

* Allowances are shown in June quarter 2017 prices, adjusted for inflation using the Stats NZ Consumers Price Index for the year ahead.

Sources: Stats NZ, the Treasury

Existing pre-commitments mean there is only $1 billion per year, on average, left to be allocated from the operating allowance for Budget 2026. Most agencies and Ministers will need to plan to manage service pressures and other commitments with little or no additional funding. Performance plans are key to managing within this constraint (Box 1). Above what is left in the operating allowance, any new funding for priority initiatives and service pressures in Budget 2026 will need to be found from savings and reprioritisation. Health, education, defence, and law and order will be priority areas in the Budget.

Box 1 - Performance plans

Performance plans are plans for each government department - and the Crown entities that fall under them - to deliver public services within existing baselines while explaining what that spending delivers and the standard it will be delivered to. The default assumption for performance plans is that there is no new funding. Performance plans, which were introduced in 2024, must be clear about trade-offs, identify performance and delivery risks and set out how these risks will be managed. They are a tool that puts the focus on medium-term sustainability and lifting performance within existing expenditure, rather than on annual Budget initiatives.

The Budget capital allowance is the amount of net new “one-off” capital funding the Government intends to allocate to capital projects in each Budget. The capital allowances for Budgets 2026, 2027 and 2028 will remain at $3.5 billion. The capital allowance for Budget 2029 has also been set at $3.5 billion.

Capital investment requirements can be large, uneven and sometimes unexpected, so the Government retains the flexibility to vary its capital allowances. This flexibility makes the capital allowances a looser constraint than the operating allowances. They are an indication of future capital spending but the biggest constraint on capital spending is the Government's debt objective.

Through the Budget 2026 capital initiatives process, more information about the capital needs and opportunities of government agencies will be provided to Ministers. The size of the capital allowances will therefore be reconsidered next year in the Budget.