Guide to New Zealand Budgeting Practices

Budget allowances

Operating allowance

The operating allowance is the pool of net new operating funding available at each Budget for new policy initiatives or cost increases in existing policies. The operating allowance can be allocated either to expenditure or revenue policy changes. Because most of the operating allowance is usually allocated to expenditure, it is often referred to as an allowance for new spending. However, Budget allowances are net concepts, where additional expenditure can be offset by savings, reprioritisation or additional revenue.

The allowance is often set in advance of Budget in accordance with the Government's fiscal strategy, and it is usually presented as an annual average amount of net new operating funding available across the current financial year (2025/26) and next four financial years (2026/27-2029/30).

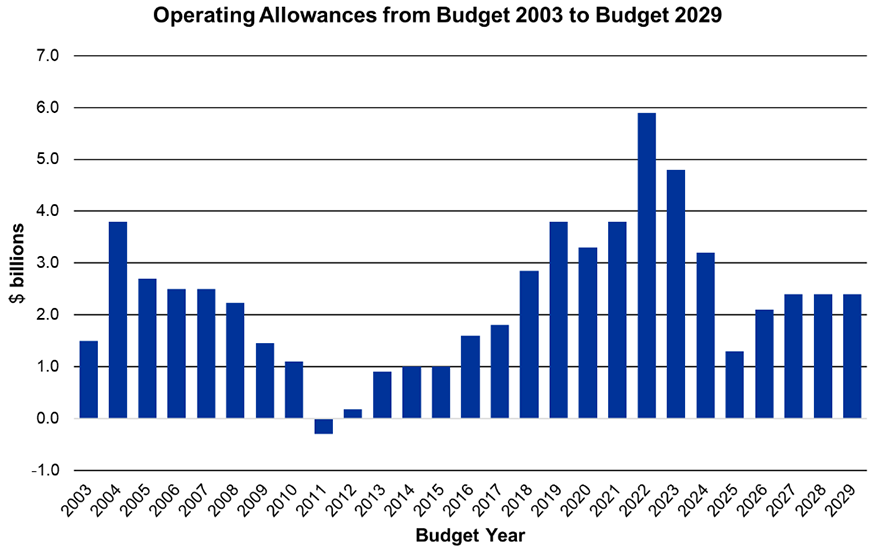

The graph below shows the average per annum operating allowances from Budget 2003 to Budget 2029.[2]

Figure 1 - Operating Allowances from Budget 2003 to Budget 2029

The operating allowance forms a self-imposed cap on expenditure growth (less any revenue changes). Because most government expenditure does not automatically adjust for inflation, it is generally expected that changes to expenses and new revenue policies are funded from the operating allowance.

However, some notable exceptions where changes to operating expenses and revenue are managed outside the operating allowance include:

- Changes in the cost of debt servicing, the Jobseeker Support benefit or tax revenue (but not tax rates) to help avoid pro-cyclical fiscal policy.[3]

- Impairments and revaluation and other changes due to large assets and liabilities (these items are highly volatile and are often non-cash).

- Previously forecast growth in expenditure, most notably New Zealand Superannuation.

In addition to creating a cap on expenditure, the allowance approach also incentivises prioritisation. The decision-making phase of the Budget process requires Ministers to discuss relative priorities and make trade-offs with the aim of forming a package of high-value initiatives that achieve their priorities and fit within allowances. This is why most new spending proposals are considered through the Budget process.

The future operating allowances are included in the fiscal forecasts to give a more accurate picture of crown spending. Budget decisions already taken are included in agency forecasts and classified into relevant areas of spend, such as health or education. Whereas decisions that are yet to be taken against future allowances are included in forecasts as new operating spend and therefore do not necessarily reflect the likely area of spend.

Operating Allowances

| $billions | Budget 2026 |

Budget 2027 |

Budget 2028 |

Budget 2029 |

|---|---|---|---|---|

| Operating allowances at the Budget Policy Statement 2026 (per annum) | 2.4 | 2.4 | 2.4 | - |

| Operating allowances set at Budget 2026 (per annum) | 2.1 | 2.4 | 2.4 | 2.4 |

| Unallocated future operating allowances | - | 2.1 | 2.4 | 2.4 |

Notes

- [2] Over time, allowances have been communicated in different ways. In some years, the Budget operating allowance has been communicated as the final outyear impact of net new operating spending and revenue policy changes. More recently, however, the Budget operating allowance has been communicated as the four-year average per annum impact. The graph shows the average per annum impact of each Budget, so the number presented may differ from the allowance that was communicated at the time.

- [3] Pro-cyclical fiscal policy is either expansionary (increased spending or tax cuts) fiscal policy in an upturn, or contractionary (reduced spending or tax increases) during a downturn. This is generally avoided in order to better manage the economic cycle. For example, if unemployment rises during a recession and the Government were to charge this cost against the operating allowance, it would crowd out other spending, which could risk exacerbating the downturn.